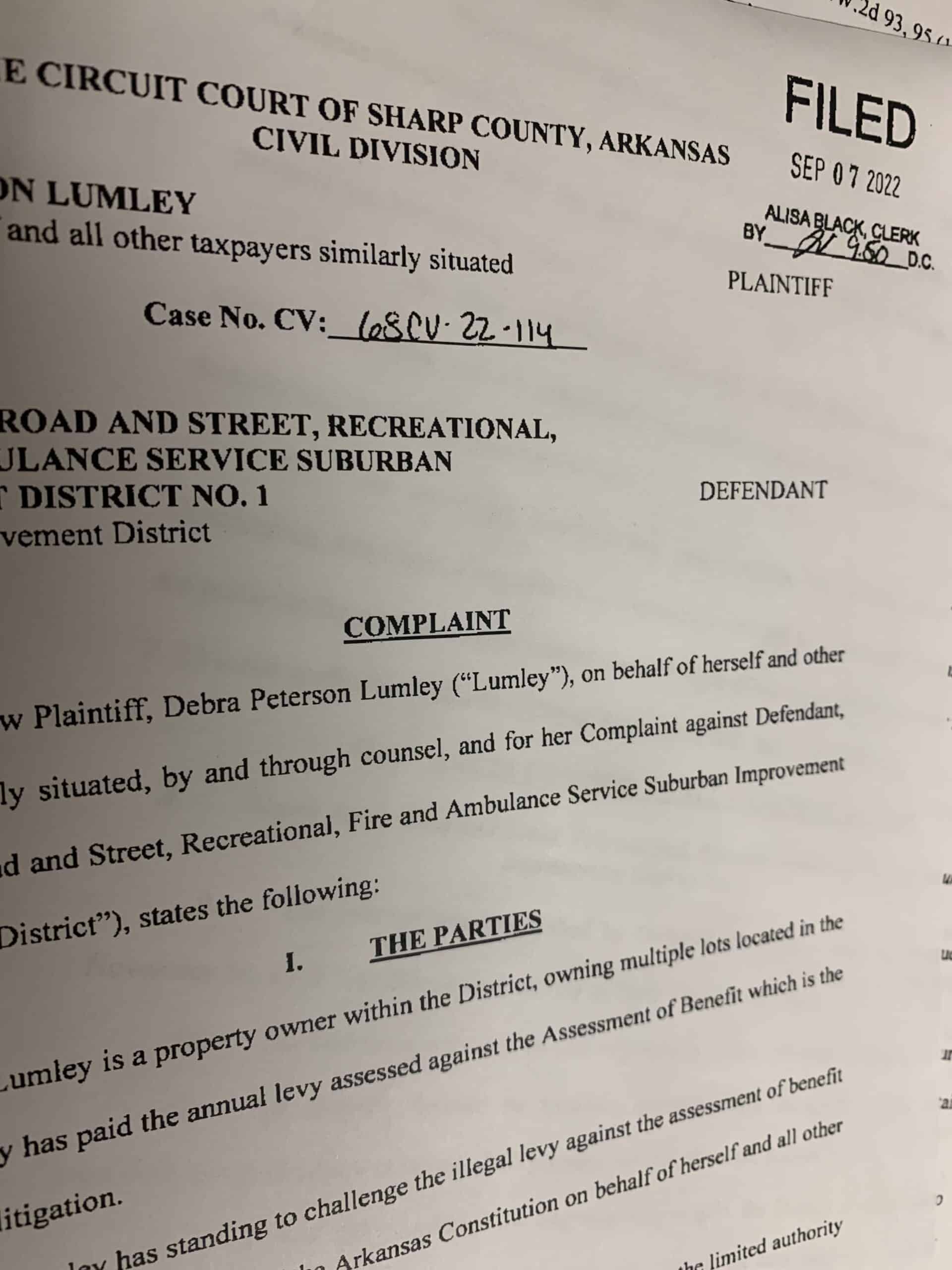

A civil lawsuit has been filed against the Ozark Acres Suburban Improvement District (OASID) as of Sept. 7 in Sharp County.

According to the documents, the suit is brought forth by resident Debra Lumley on behalf of herself and all other taxpayers similarly situated.

The suit was filed by attorneys Timothy Hutchinson, Larry McCredy and Bo Renner of RMP LLP, the same company who was involved in the recently settled lawsuit against the Cherokee Village Suburban Improvement District, American Land Company and City of Cherokee Village.

In the suit, the primary complaint revolves around the annual levy assessed against the Assessment of Benefits which is being challenged.

According to the suit, “The District does not have general taxing authority, but only limited authority permitted by statute..,” the suit reads. “The District has, therefore, assumed the status of a de jure governmental agency.”

The suit goes on to state several statutes which may be familiar to those who followed the recent suits against Cherokee Village, Holiday Island and other communities with suburban improvement districts.

On Nov. 16, 1979, the district was established by order of the Sharp County Court and was formed for limited purposes.

Through its appointed commissioners, certain gifts of improvements or facilities were accepted.

In 1980, the assessment of benefits was adopted for the District and since that time, has been the basis for the annual tax levied against the Assessed Benefits.

“As such, each year since 1981, the property owners paid down the Assessed Benefit for their separately owned parcels through the payment of an annual installment. Since 1981, the district has not added any other improvements nor has a reassessment of benefits been adopted,” the suit states. “Beginning in 1981, the defendants levied an annual installment in the amount of 10 percent of the Assessment of Benefit each year. Being able to charge interest at a rate no greater than 6 percent principal on the Assessed Benefit was, at the least, reduced by four percent for each year since 1981. As such, the Assessed Benefit was fully exhausted within 25 years of its enactment (2006).”

The OASID has continued to collect against parcels that paid off the Assessment of Benefits in 2006 and as of a recent OASID meeting, the 2023 levy has been reduced from 10 percent to eight percent.

For relief sought, the suit requests an order declaring the defendants annual installment against the Assessment of Benefits be completely exhausted for the properties that are not delinquent and prohibiting the district from further exhaustion and/or collection of a levy against the Assessment of Benefits for parcels that have paid each year’s annual installment; an order finding the plaintiff and all similarly situated taxpayers are entitled to a declaratory judgment declaring which parcels have paid off the Assessment of Benefits and the amount for remaining parcels; a refund of all moneys collected on any levy charged after the Assessment of Benefits for any particular parcel was already exhausted and that the plaintiff and all similarly situated taxpayers are further entitled to an award of reasonable attorney fees and costs of collection as allowed for under Arkansas law.

As of Sept. 10, the attorney for the OASID had not yet been served a copy of the suit and no special meeting has been called by the OASID by commissioners to discuss the issue.

Lauren is a an award-winning journalist who decided after 10 years of newspaper experience to venture out. Hallmark Times was born.

{kind=link}

{kind=link}

{kind=link}

{kind=link}